SEA-LNG has published a report entitled ‘“The Journey: A Decade Moving Towards a Cleaner Future”, which analyses the ten-year development of LNG as a marine fuel and its role in the decarbonisation of shipping. The document examines the sequential path to reducing emissions in the industry — from liquefied natural gas (LNG) to liquefied biomethane (Bio-LNG) and e-methane.

SEA-LNG has published a report entitled ‘“The Journey: A Decade Moving Towards a Cleaner Future”, which analyses the ten-year development of LNG as a marine fuel and its role in the decarbonisation of shipping. The document examines the sequential path to reducing emissions in the industry — from liquefied natural gas (LNG) to liquefied biomethane (Bio-LNG) and e-methane.

The report assesses the current state of the LNG fleet and infrastructure, investment dynamics, regulatory context, and prospects for scaling up renewable and synthetic gases. Particular focus is given to the role of Bio-LNG and e-methane in achieving maritime transport climate goals and shaping a long-term strategy for the transition to low-carbon shipping.

A decade of growth: LNG as the first stage of transition

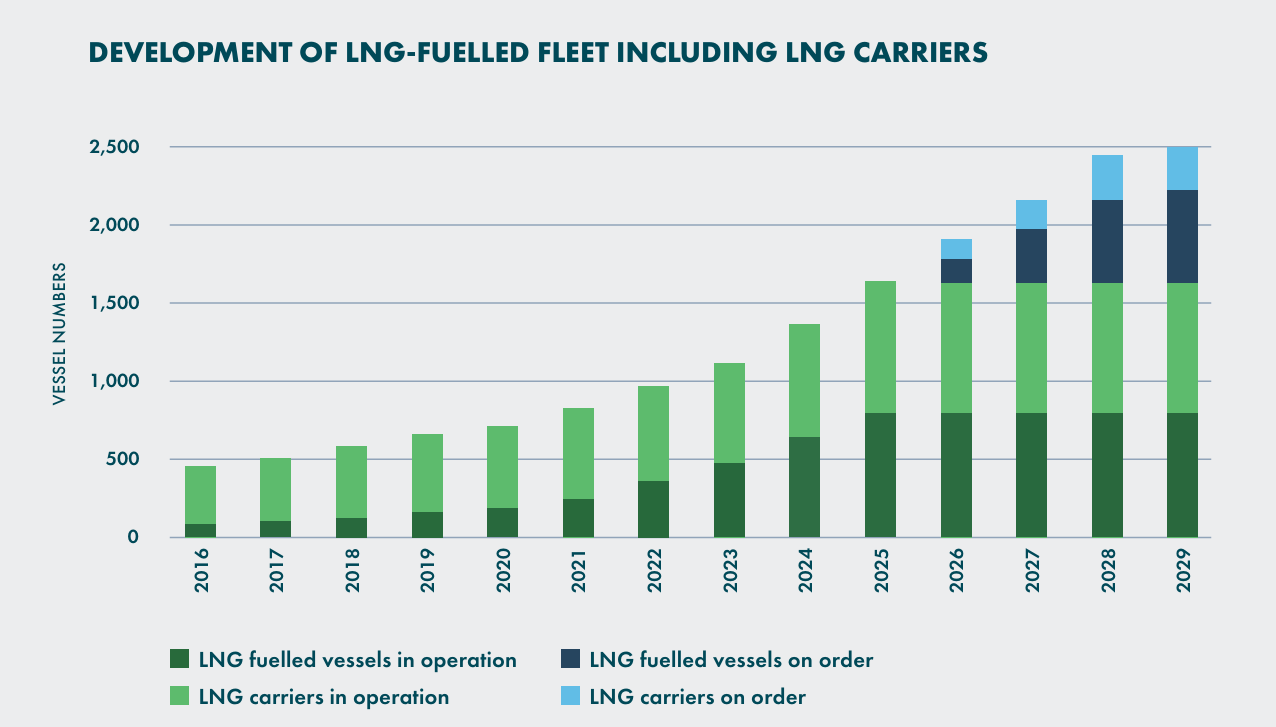

Since SEA-LNG was founded in 2016, LNG has gone from a niche to a mainstream solution for maritime with numbers of vessels using LNG as a marine fuel increasing 10-fold to 850 vessels in operation with a further 642 on order. In total, the LNG fleet (in operation and on order) already exceeds 10% of the global fleet.

Source: SEA-LNG DNV AFI.

Despite an overall decline in orders for new vessels (from 551 in 2024 to 275 in 2025), LNG’s position has only strengthened: 79% of all orders for alternative fuel vessels are for LNG, primarily in the ultra-large container ship segment.

LNG bunkers are now available in 222 ports with plans for a further 62. Investment in LNG dual fuel vessels and the associated fuel supply chains over the past 10 years has amounted to more than $150 billion.

The advantages of methane

The methane molecule’s advantages over other alternative marine fuels such as methanol and ammonia include:

- higher energy density;

- widespread fuel availability;

- lower costs of regulatory compliance and the commercial optionality it offers;

- “inoculating” itself against regulatory uncertainty.

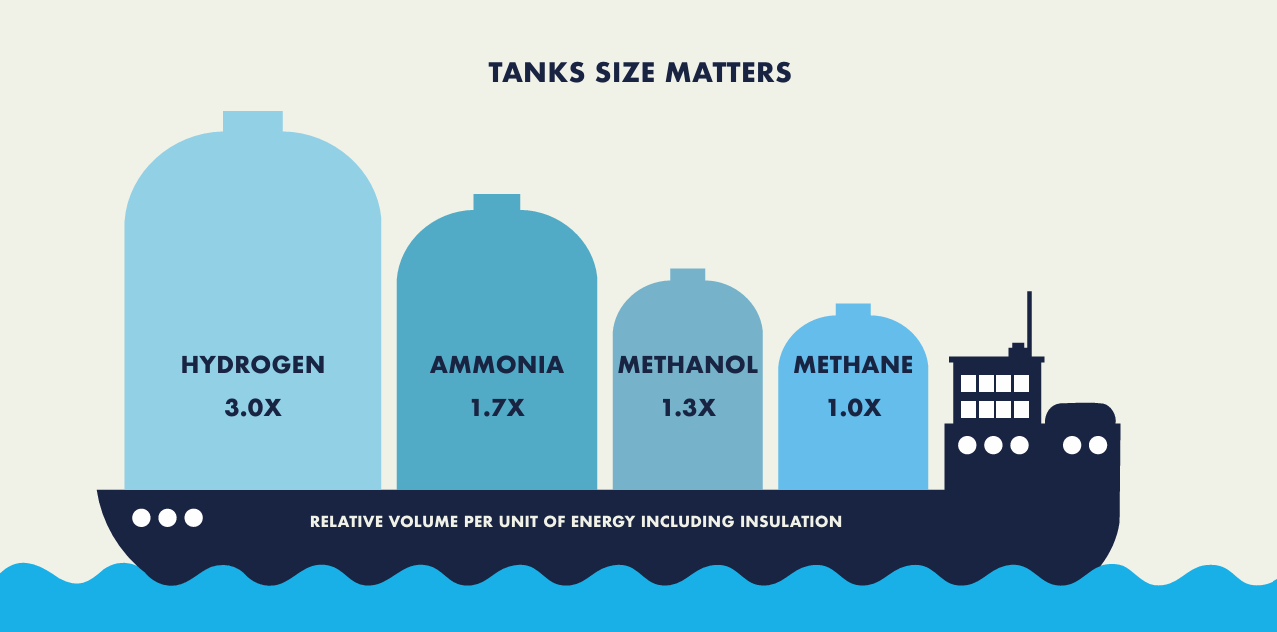

Taking into account the insulation requirements for tanks, methane has the highest energy density among the alternatives. Methanol will require a tank 1.3 times larger, for the same amount of energy and the multiples for liquefied ammonia and hydrogen are 1.7 and 3.0 respectively. These parameters directly affect the commercial efficiency of ships and make methane a technologically and economically attractive solution.

Source: SEA-LNG Analysis.

The next step in decarbonisation: liquefied biomethane

Liquefied biomethane (Bio-LNG) produced from sustainable biomass resources such as agricultural and municipal waste, is a central next step along the methane runway towards decarbonisation. It is virtually identical chemically to LNG, and fully compatible as a drop-in fuel in existing LNG engines with no blending issues. This means that the transition to renewable gas can take place without technical barriers and without risks for fleet operators.

Scaling and climate effect

It is estimated that biomethane production could increase 20-fold by 2050. Once demand from other sectors is taken into account liquefied biomethane has the potential to play a significant role in decarbonizing shipping. If used in the form of a 20% blend with LNG, it could cover up to 16% of global shipping demand by 2030.

Emissions reduction will depend on how the liquefied biomethane is produced and the engines in which it is used. In general, the use of liquefied biomethane as a marine fuel can reduce GHG emissions by up to 80% compared to marine diesel on a full well-to-wake basis. When produced from the anaerobic digestion of waste materials, such as manure, methane that would otherwise be released into the atmosphere is captured, resulting in negative emissions of up to -190% compared with diesel.

However, the IEA’s May 2025 report, ‘Outlook for Biogas and Biomethane’ states that biomethane is an underutilised resource in the energy transition. It is currently growing at a rate of 20% per annum and the IEA estimates some one trillion cubic metres of biomethane could be produced every year using organic waste streams (this would be the equivalent of around 25% of the total global natural gas demand today) yet only around 5% of the total potential for biogas and biomethane production is currently being utilised.

The opportunities for greater production of Bio-LNG are significant and will be exploited given the obvious commercial and environmental benefits.

European momentum

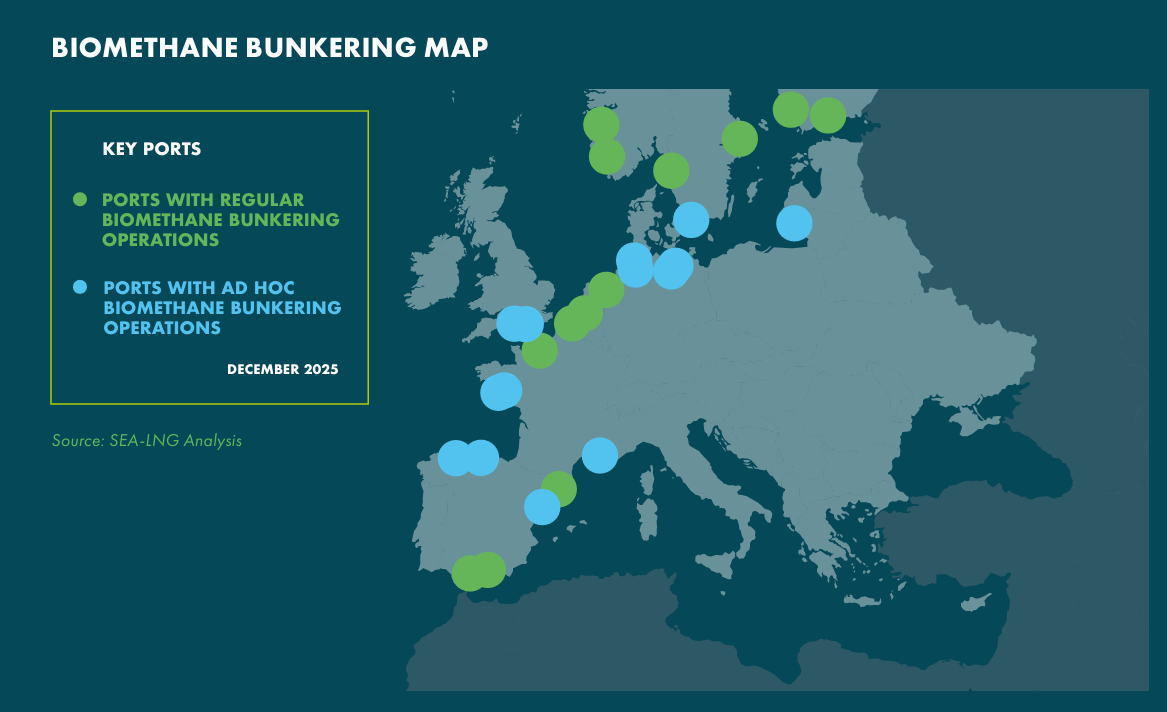

Source: SEA-LNG Analysis.

In 2025, Europe is experiencing a boom in Bio-LNG bunkering. This is a response by shipping companies to stricter EU regulations (in particular FuelEU Maritime) and significant financial incentives to reduce emissions.

Bio-LNG bunkering operations have already been carried out in key ports in Belgium, France, Finland, Italy, Lithuania, the Netherlands, Norway, Spain, Sweden and the United Kingdom, with at least 10 major suppliers involved.

Bio-LNG is used in various segments, from cruise ships and container ships to tankers, ferries and support vessels.

E-methane: a synthetic path to zero emissions

E-methane, a synthetic fuel produced using renewable electricity and green hydrogen. It can be used with existing LNG infrastructure (including bunkering), making it a commercially viable investment for long-term compliance.

E-methane retains:

- high energy density;

- normal storage conditions;

- established safety procedures;

- stable vessel performance.

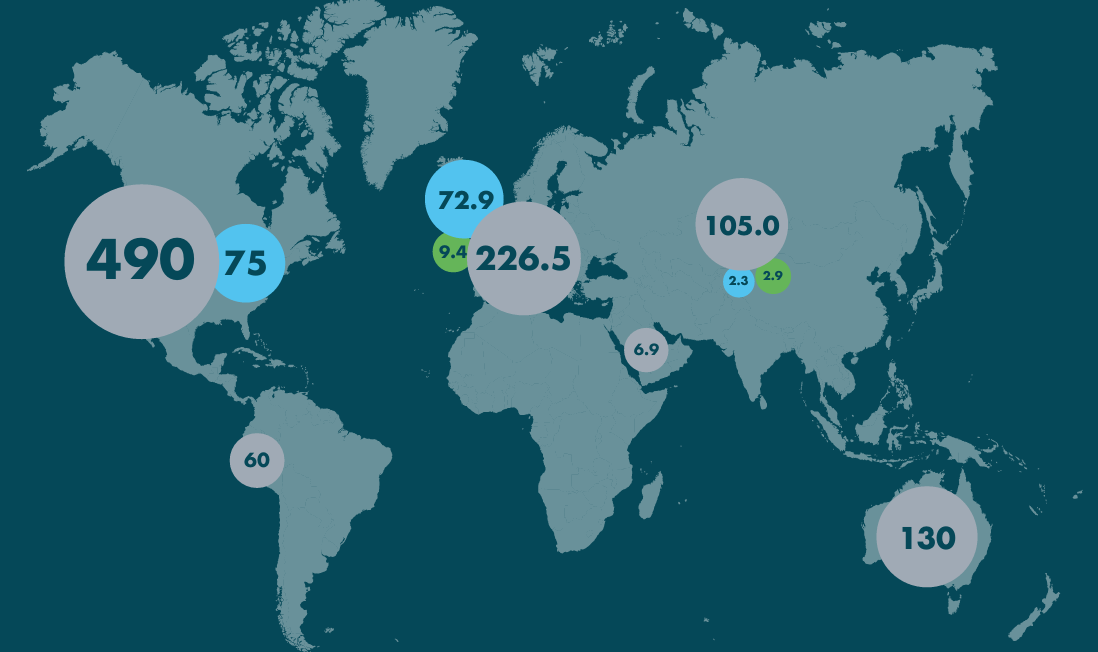

E-methane project development continues in Europe, North America, South America, Australia and Asia driven by demand from utilities. Some 150kt pa of capacity is in FEED and a further 1 Mtpa at a pre-feasibility / feasibility stage.

Map of key e-methane production projects. Capacity (kilotons per year): in operation (green), under constraction/FEED stage (blue), pre-feasibility/feasibility studies (grey). Source: e-NG Coalition.

Regulatory context and global perspective

The IMO’s decision in October 2025 to postpone the adoption of the Zero Emissions Framework Agreement provoked a mixed reaction on the market. At the same time, the industry demonstrated its ability to quickly adapt to new requirements.

SEA-LNG is calling for a single global decarbonisation framework based on regulations which are goal-based and technology neutral, which protect first movers and which incentivise solutions that are practical, scalable and investable.

Conclusions

Over the past decade, a large-scale infrastructure and investment base has been formed to reduce emissions in maritime transport based on methane solutions, and 2025 has become a key milestone in defining a clear trajectory for their further development in shipping. Large-scale LNG infrastructure has already been created, Bio-LNG bunkering is becoming common practice, and e-methane is gradually moving from the concept phase to the stage of real investment projects. For maritime transport, this means the formation of a long-term, technologically coherent, and economically sound model for the transition to climate neutrality.

Download the full report by SEA-LNG

‘2025 is the year the methane decarbonisation pathway became a clear runway. The year our advocacy for LNG as a fuel in transition from fossil LNG through liquefied biomethane (Bio-LNG ) to liquefied e-methane took off, with record amounts of Bio-LNG powering global shipping today and growing strongly into the future’, — COO, SEA-LNG.