In September 2025, the European Biogas Association (EBA) published a comprehensive document exploring the potential use of biogenic CO2 from the biogas sector. This would allow the EU to implement its strategy to reduce carbon emissions and support the sustainable development of a low-carbon economy as a scalable and competitive solution.

This white paper examines the current status and future outlook of biogenic CO2 carbon capture, utilisation and storage (CCUS) from both the technical and economic perspectives, as well as providing market intelligence on trends shaping bioCO2 capture. The report details the sector’s fast-growing capture capacities, the expanding range of applications for renewable CO2 and the policy frameworks guiding its scale-up.

Biogenic CO2

Biogenic CO2 is the carbon dioxide (CO2) resulting from the decomposition, digestion, chemical reaction or combustion of biomass-derived products. Atmospheric CO2, assimilated by biomass through photosynthesis, is subsequently returned to the atmosphere or the soil as biogenic CO2, depending on the type of conversion and final use of the biomass, in what is known as the natural short carbon cycle.

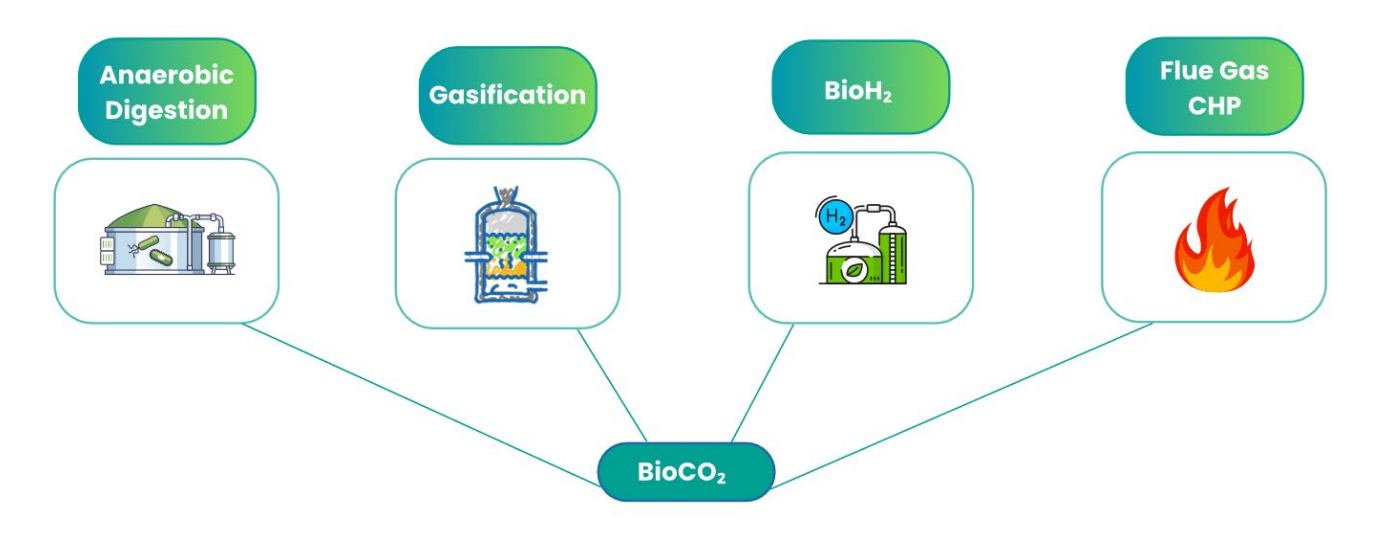

Sources of biogenic CO2 from the biogas sector. Source: EBA.

Biogenic CO2 for Europe

Biogenic CO2 from biogas presents an immediate and scalable solution to Europe’s growing climate and circularity ambitions. The current conventional CO2 demand in Europe in 2024 stands at 13.9 Mt/year, with the merchant market accounting for 56% of this total.

However, the European Commission’s Impact Assessment for the Climate Target projects that emerging markets (primarily e-fuels and storage) will require a dramatic increase to 344 Mt of CO2 by 2040 to support a 90% net reduction in GHGs.

E-fuels alone are likely to require over thirteen times today’s merchant CO2 volumes within just 15 years, demonstrating an urgent need to scale up sustainable, non-fossil CO2 sources.

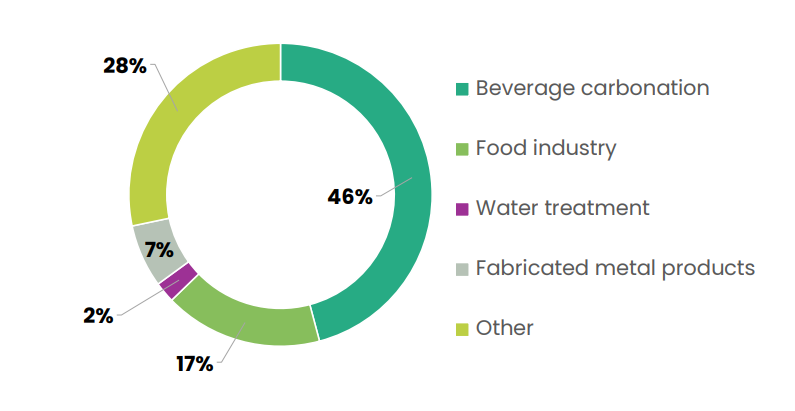

European CO2 consumption of liquid and solid CO2 by end use based on S&P Global (2024). Source: EBA.

By 2040, the technical potential of biogenic CO2 from anaerobic digestion in the EU-27 is estimated to reach 89 Mt annually, which is sufficient to cover more than 25% of the necessary carbon capture to meet the Climate Law objective. Biogenic CO2 capture is already being implemented in the biogas sector, primarily through the production of biomethane.

In addition to the biogas sector, other sources include bioethanol production and biomass combustion, as well as direct air capture, which can also ensure sustainable CO2 production.

Compared to other methods of sustainable CO2 production, the biogas sector offers one of the most efficient, economical and scalable solutions for CO2 capture.

Biomethane and bio-CO2

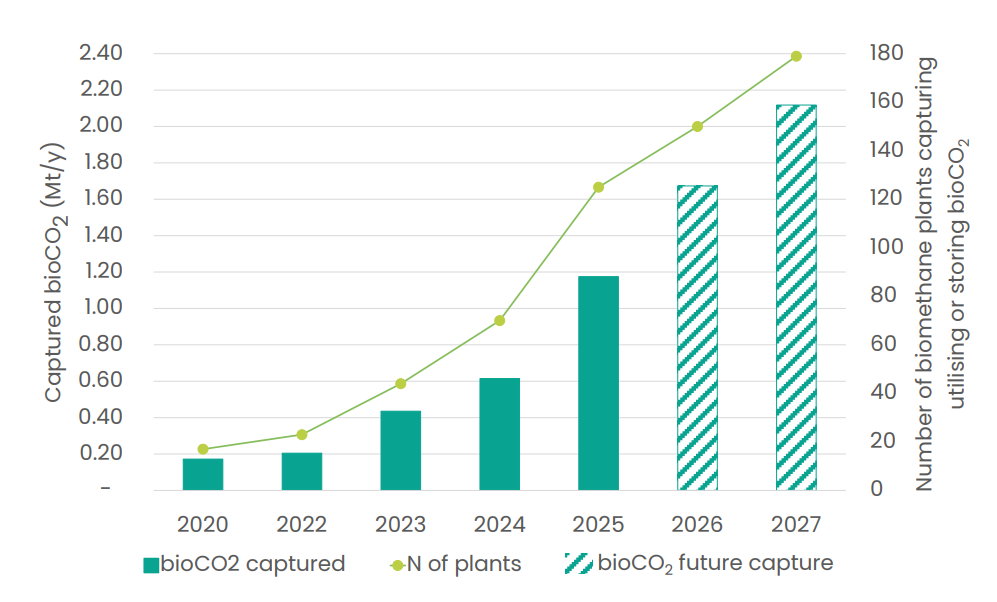

The market data study shows the number of biomethane plants capturing biogenic CO2 in Europe has increased eightfold over the past five years, from 15 plants capturing 0.16 million tonnes in 2020 to 125 plants capturing 1.17 million tonnes in 2025, equivalent to around 14% of Europe’s merchant liquid and solid CO2 demand. With confirmed and underconstruction projects, capacity is expected to exceed 2 Mt annually by 2027, with 179 biomethane plants.

Historical and projected captured biogenic CO2. Source: EBA.

Biomethane production capacity varies significantly across Europe, with countries such as Denmark and Sweden typically operating larger scale facilities, whereas others, including Finland, Switzerland and France, predominantly operate smaller-scale plants. By 2027, 31% of facilities are expected to have a capture capacity of less than 5,000 t CO₂/y, i.e. below the average biomethane plant size (483 Nm3/h) in Europe.

The United Kingdom currently leads in biogenic carbon capture, accounting for 22% of the total amount captured at present. It is followed by Germany (15%), Denmark (14%), France (14%), the Netherlands (12%) and Italy (12%).

Conclusions

To fully unlock the potential of biogenic CO₂, Europe must tackle policy and infrastructure barriers, prioritising bioCO₂ as a premium resource for net-zero and negative emissions pathways. There is a strong need for targeted incentives, integrated CO₂ infrastructure, harmonised certification and traceability schemes, and the expansion of support measures that reflect bioCO₂’s superior sustainability value.

To deliver climate, circularity and competitiveness benefits for Europe, biogenic CO₂ from the biomethane sector must be the cornerstone of Europe’s energy transition.

Download the EBA report on biogenic CO2

EBA fully believes in the future potential of renewable gas in Europe. Founded in 2009, the association is committed to the deployment of sustainable biogas and biomethane production and use throughout the continent. EBA counts today on a well-established network of over 300 national associations and other organisations covering the whole biogas and biomethane value chain across Europe and beyond.